TL;DR — Quick Summary

- ACH costs 70-90% less than card processing for B2B transactions over $1,000.

- ACH settlement takes 1-3 business days, compared to instant card authorization.

- B2B merchants processing over $50,000 monthly should evaluate ACH as a primary payment method.

- ACH reduces fraud by up to 90% compared to card transactions, but requires customer authorization.

What Is ACH and Why It Matters for B2B Payments

ACH (Automated Clearing House) is an electronic network for financial transactions in the United States. While consumers commonly use ACH for direct deposit and bill pay, B2B merchants are increasingly adopting ACH as a lower-cost alternative to card processing for large-ticket transactions.

According to Nacha, the organization governing ACH, the network processed 30.8 billion transactions in 2025 with a total value of $76.7 trillion. B2B payments represent the fastest-growing segment, driven by merchant demand for lower processing fees on high-value transactions.

ACH vs Card Processing: Direct Comparison

| Feature | ACH | Credit Card |

|---|---|---|

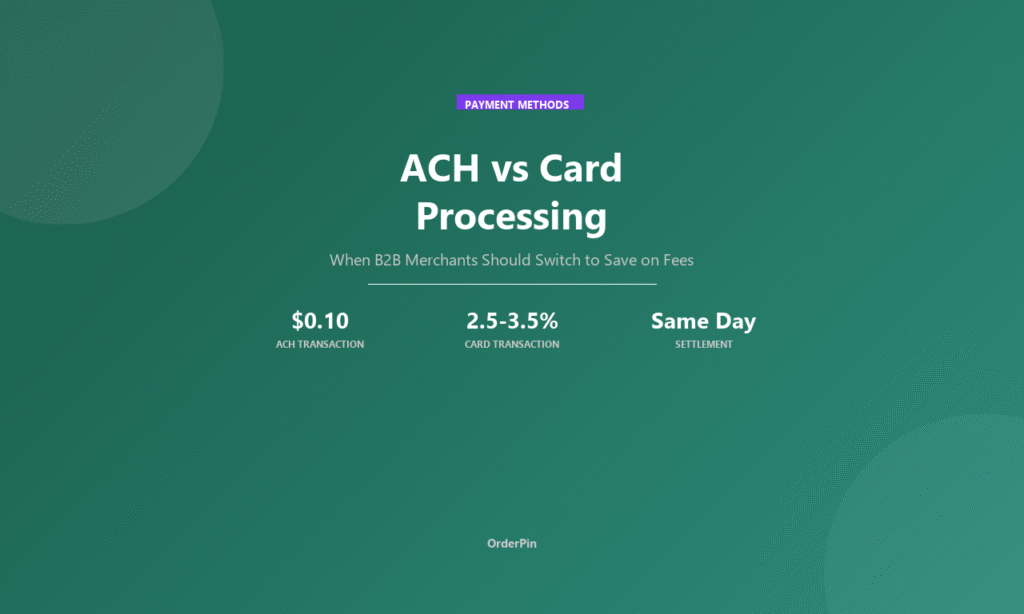

| Transaction fee | $0.10-0.30 | 0.30-3.0% |

| Settlement time | 1-3 business days | Instant |

| Fraud liability | Very Low | Moderate |

| Chargeback risk | Very Low | High |

| Transaction limits | $1M/day typical | Varies |

| Customer authorization | Bank verification required | Card present/not required |

When ACH Makes Sense: The $50K Threshold

For B2B merchants, ACH becomes financially attractive at approximately $50,000 in monthly card transaction volume. At this threshold, the math favors ACH:

- $50,000/mo card volume: ~$750-1,500/month in fees (at 1.5-3%)

- Same volume via ACH: ~$50-150/month (at $0.10-0.30/transaction)

- Monthly savings: $700-1,450, or $8,400-17,400/year

The Trade-off: Settlement Delay

ACH takes 1-3 business days to settle, while cards authorize instantly. For businesses with tight cash flow or inventory needs, this delay can be problematic. Consider offering both ACH and card options, letting customers choose based on their priorities.

How ISOs Can Win with ACH Solutions

ISOs who offer ACH processing alongside card services gain a competitive advantage in B2B verticals:

- Target high-volume B2B merchants: Wholesale distributors, manufacturers, and service companies processing $50K+/month

- Position as cost savings expert: Quantify potential savings in dollars, not percentages

- Offer hybrid acceptance: Let merchants accept both, optimizing by transaction size

- Highlight fraud reduction: Especially valuable for industries with high chargeback rates

How OrderPin Supports ACH for B2B Merchants

Frequently Asked Questions

Conclusion

ACH processing represents a massive opportunity for ISOs serving B2B merchants. With fees 85% lower than card processing and fraud reduced by up to 90%, the value proposition is clear for merchants processing over $50,000 monthly.

The key is positioning: not as a replacement for cards, but as a complementary payment method that saves money on high-value transactions. Merchants who offer both ACH and cards capture the benefits of each while giving customers choice.

About OrderPin

OrderPin is a white-label POS platform built for ISO and MSP partners. We offer integrated ACH and card processing with smart routing, instant bank verification, and automatic optimization for B2B merchants — all under your own brand with full data ownership.