TL;DR — Quick Summary

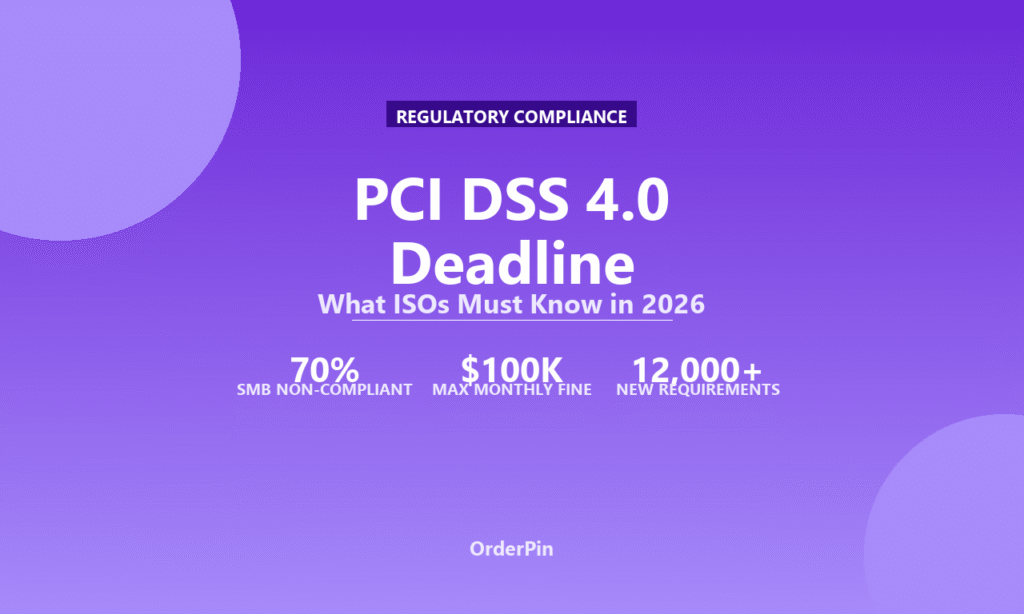

- PCI DSS 4.0 became the only valid standard on March 31, 2025 — and an estimated 70% of SMB merchants are still running non-compliant POS systems.

- The window for compliant migration is closing fast: non-compliant merchants face fines of up to $100,000 per month and increased risk of data breaches that can destroy a business.

- ISOs who position themselves as PCI compliance partners — not just POS vendors — are capturing new revenue streams while solving a real existential problem for their merchants.

PCI DSS 4.0 Is Here — And Most Merchants Are Not Ready

On March 31, 2025, PCI DSS version 3.2.1 officially retired. From that date forward, the Payment Card Industry Data Security Standard version 4.0 became the only valid framework for any business that stores, processes, or transmits cardholder data. This was not a soft deadline or a gentle transition period — it was a hard cutoff. And yet, according to industry surveys conducted in late 2024 and early 2025, an estimated 70% of small and medium-sized business merchants are still operating with POS systems and security practices that do not meet the 4.0 standard.

For ISOs, this compliance gap represents both a significant risk for their merchant base and one of the most compelling revenue opportunities of the decade. Merchants who need to upgrade their POS systems, update their security infrastructure, and bring their card processing environment into compliance are actively looking for trusted advisors — and their current ISO is ideally positioned to be that advisor, if they understand what 4.0 actually requires.

What Changed in PCI DSS 4.0: The Key Differences ISOs Must Know

PCI DSS 4.0 is not just a version number bump — it represents the most significant overhaul of the standard since version 3.0 in 2013. The new standard introduces 64 new requirements and significantly strengthens existing ones. Understanding what changed is essential for ISOs who want to have informed conversations with their merchants about compliance gaps and upgrade paths.

1. Customized Approach Introduced

One of the most significant changes in 4.0 is the introduction of the Customized Approach. Rather than strictly following every written requirement as written, qualifying organizations can now implement a customized control that meets the stated objective, provided it is validated by a Qualified Security Assessor (QSA). This gives large enterprises more flexibility but requires significantly more documentation and validation — making compliance support from experienced ISOs more valuable than ever.

2. Targeted Risk Analysis

Version 4.0 replaces many scheduled activities with a risk-based approach. Organizations must now perform a targeted risk analysis to determine the frequency of certain activities — meaning merchants who can demonstrate strong security postures may be able to reduce some compliance burdens, while those with weaker security will face more frequent testing and review requirements.

3. Enhanced Authentication Requirements

Multi-factor authentication (MFA) is now required for all access to the cardholder data environment — not just for remote access as in 3.2.1. This is one of the most operationally significant changes: many SMB merchants have POS systems where a single login grants broad access, and getting all staff onto MFA-compliant authentication systems is a non-trivial IT project.

4. Expanded Encryption Requirements

4.0 strengthens requirements around how cardholder data is encrypted both at rest and in transit. Merchants who implemented encryption five or more years ago may find their encryption methods no longer meet current cryptographic standards — requiring hardware or software upgrades that go beyond simply updating POS firmware.

5. Greater Emphasis on Scripts and Automated Tools

4.0 acknowledges that many attacks now originate from malicious scripts running in web browsers and point-of-sale terminals. New requirements specifically address script inventory management, script integrity validation, and endpoint protection — areas that many traditional POS setups do not adequately address.

6. STRONG Authentication for Admin Access

Password requirements have been significantly strengthened: minimum password length increased to 12 characters (from 8), and passwords must be changed every 90 days unless a risk-based analysis determines otherwise. For many SMB merchants with informal IT practices, this requires real process changes, not just technology updates.

Frequently Asked Questions

What exactly happened on the March 31, 2025 PCI DSS deadline?

March 31, 2025 was the official end-of-life date for PCI DSS version 3.2.1. After this date, all organizations assessed against PCI DSS must be compliant with version 4.0. There was no extension granted. The Payment Card Industry Security Standards Council (PCI SSC) made this deadline clear years in advance, but industry surveys suggest the majority of SMBs did not begin meaningful preparation until 2024 — leaving many scrambling to catch up. Organizations that continue to process card payments under a 3.2.1 compliance framework after this date are technically out of compliance.

Who actually enforces PCI DSS compliance — and what are the real consequences of non-compliance?

PCI DSS compliance is not a law — it is a contractual obligation enforced by the payment card brands (Visa, Mastercard, Amex, Discover) through the acquiring banks (processors, ISOs). Consequences include: contractual fines from card brands ($5,000-$100,000 per month from Visa and Mastercard for persistent non-compliance), increased processing fees for non-compliant merchants, liability for fraud losses if a breach occurs at a non-compliant merchant, potential termination of card processing capability, and in extreme cases, costly breach investigations and lawsuits. The fines flow through the acquiring bank to the merchant, but the reputational damage — particularly for an ISO whose merchant base has widespread compliance failures — can be far more damaging than the fines themselves.

What are the most expensive changes SMB merchants need to make for 4.0 compliance?

For most SMB merchants, the most costly changes are: (1) POS hardware replacement — older terminals that cannot support 4.0 cryptographic standards or MFA requirements must be replaced, typically $300-$1,500 per terminal; (2) Network infrastructure updates — segmented networks, updated firewalls, and wireless security upgrades often run $5,000-$30,000 for a multi-lane retail location; (3) MFA implementation — rolling out multi-factor authentication across all employees with access to payment systems requires software licensing, hardware tokens or authenticator apps, and IT labor; (4) QSA assessment costs — for merchants who require a formal Report on Compliance (ROC), QSA fees typically range from $20,000-$100,000+ depending on scope; (5) Penetration testing — required annually under 4.0 vs. every three years under 3.2.1, running $10,000-$50,000 per engagement.

How can ISOs help their merchants achieve PCI DSS 4.0 compliance?

ISOs have several distinct advantages in helping merchants with compliance: (1) They can introduce compliant POS solutions as a bundle — choosing terminals and software platforms that are pre-validated against 4.0 requirements; (2) They can partner with PCI compliance service providers and earn referral revenue while solving merchant problems; (3) They can bundle compliance services — monitoring, MFA, network security — into their ISO value proposition, creating recurring revenue streams; (4) They can conduct informal pre-assessments using PCI SSC’s Self-Assessment Questionnaires (SAQs) to identify gaps before they become costly problems; (5) They can guide merchants toward PCI-validated payment applications (VPA) and point-to-point encryption (P2PE) solutions that reduce the merchant’s compliance scope and burden. The key is positioning yourself as a compliance partner, not just a POS vendor — merchants who trust you with their compliance are merchants who will never switch to a competitor.

What is the difference between a SAQ and a full ROC assessment for PCI compliance?

Most SMB merchants will satisfy their PCI DSS compliance requirements through a Self-Assessment Questionnaire (SAQ) — a document the merchant completes to attest to their own compliance. There are multiple SAQ types (SAQ A, A-Ent, B, B-IP, C-VT, C, D, P2PE-HW), and choosing the right one is important: using the wrong SAQ type leaves merchants potentially attesting to requirements they do not actually meet. A Report on Compliance (ROC) conducted by a Qualified Security Assessor (QSA) is required for merchants with over 300,000 annual Visa/Mastercard transactions (Level 1 and 2 merchants). The ROC is far more rigorous and expensive, but it provides a higher level of assurance. For most ISO merchants, the ROC is not required — but the SAQ process should still be taken seriously, because attesting to requirements that are not actually in place is itself a compliance violation.

How ISOs Can Turn Compliance Into a Revenue Opportunity

The merchants who are struggling with PCI DSS 4.0 compliance are not just a risk — they are a business opportunity. Here is how forward-thinking ISOs are turning compliance challenges into customer relationships and recurring revenue.

Package Compliance Into Your ISO Value Proposition

The merchants most at risk of non-compliance are often the ones who have the least internal IT expertise. They chose their POS system years ago, it has been working fine, and they did not even know there was a new compliance standard. These merchants need a trusted advisor — and if you do not step into that role, someone else will. Position your ISO as the partner who understands the 4.0 standard, can assess their current compliance posture, and can provide a clear upgrade roadmap.

Partner with Compliance-as-a-Service Providers

You do not need to become a PCI QSA to provide meaningful compliance value to your merchants. The market has a growing number of Compliance-as-a-Service (CaaS) providers who specialize in helping SMBs navigate PCI DSS 4.0: continuous network monitoring, vulnerability scanning, MFA deployment, SAQ completion support, and QSA liaison services. Establish referral relationships with 2-3 of these providers and earn referral fees while solving merchant problems.

Prioritize Your High-Risk Merchant Segment

Not every merchant is equally at risk — and not every merchant is equally valuable. Focus your compliance outreach on merchants who: process the highest transaction volumes (they have the most to lose from a breach and the highest compliance burden), operate in industries with the highest breach rates (retail, restaurants, hospitality), use older POS hardware or legacy payment software, or have previously reported security incidents or concerns. These merchants will be the most receptive to compliance support — and converting them into compliance-aware, compliant merchants dramatically increases their lifetime value.

Build Compliance Scoping into Every New Merchant Onboarding

Going forward, every new merchant you onboard should receive a PCI DSS compliance scoping assessment as part of your standard onboarding process. This ensures compliance is built into the foundation of the relationship — not retrofitted after problems emerge. Document their SAQ type, identify which requirements are already met by their environment, and provide a clear roadmap for meeting any gaps. This positions your ISO as a compliance-first partner from day one.

How OrderPin Helps ISOs Deliver PCI DSS 4.0 Compliance

PCI-Validated Payment Platform

OrderPin is a PCI-validated payment application (VPA) and supports P2PE (Point-to-Point Encryption) deployment — dramatically reducing the compliance burden for ISOs and their merchants compared to legacy POS solutions.

Built-In MFA and Secure Authentication

OrderPin’s platform natively supports multi-factor authentication, role-based access controls, and automated security logging — meeting key 4.0 requirements out of the box without expensive third-party add-ons.

Reduced Compliance Scope

Merchants using OrderPin’s P2PE solution can qualify for SAQ P2PE-HW — one of the simplest and lowest-scope SAQ types — dramatically reducing their ongoing compliance burden and cost.

Conclusion: Compliance Is the Ultimate Retention Strategy

PCI DSS 4.0 compliance is not just a security issue — it is a business relationship issue. Merchants who trust their ISO to guide them through 4.0 compliance are merchants who have chosen a partner, not just a vendor. That relationship — built on expertise, guidance, and shared responsibility for security — is the strongest retention mechanism in the payments industry.

The compliance gap that exists today is an opportunity. 70% of SMB merchants are non-compliant. They need help. The ISOs who step in — with the right knowledge, the right partners, and the right platform — will turn compliance risk into loyalty, recurring revenue, and a competitive moat that direct platforms like Square and Shopify simply cannot match.

The deadline has passed. The non-compliance gap is real and growing. This is the moment for ISOs to lead — and OrderPin is the platform that makes that leadership possible.

About OrderPin

OrderPin is a white-label POS platform for ISO and MSP partners. Our PCI-validated, P2PE-capable platform reduces compliance burden for ISOs and their merchants — while providing the modern payment experience that merchants demand. Learn more about OrderPin’s ISO partner program