TL;DR — Quick Summary

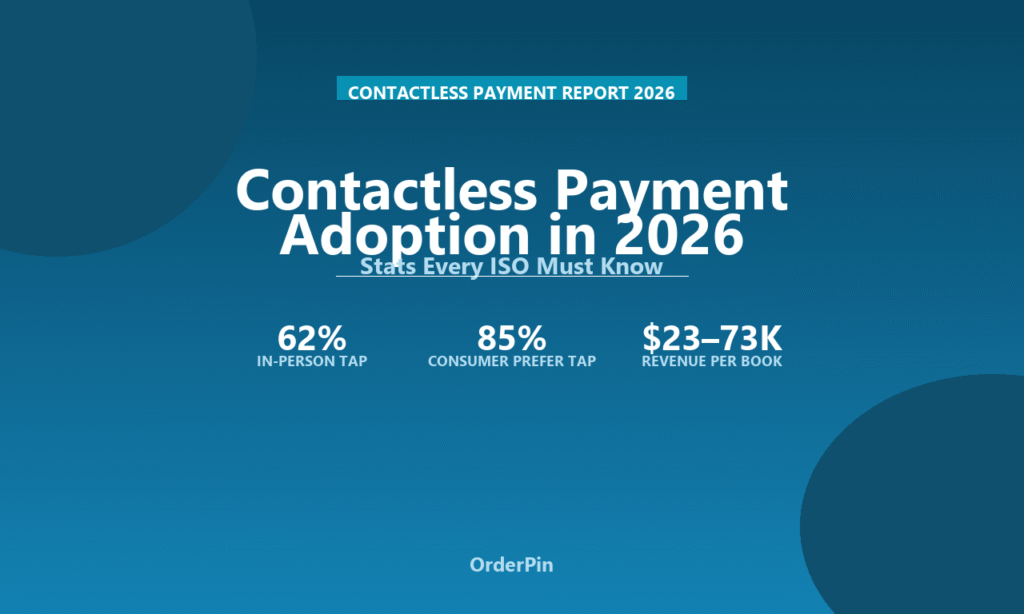

- Contactless payments now account for 62% of all in-person card transactions in the U.S., up from 38% in 2022 — driven by consumer habit and Tap to Pay on iPhone/Android.

- Merchants without NFC-enabled terminals risk losing 15–22% of younger customers who choose a competitor over swiping or inserting a card.

- ISOs must phase out non-NFC terminals by 2027, upgrade to SoftPOS-capable devices, and educate merchants that contactless is no longer optional.

The tap-to-pay revolution is past the tipping point. In 2026, contactless payments — near-field communication (NFC) tapping with cards, phones, and wearables — have become the dominant way Americans pay in person. And the shift is accelerating faster than most ISOs realize.

This article gives ISOs the data they need to convince merchants to upgrade terminals, adopt SoftPOS, and understand why contactless is no longer an optional feature — it is the baseline expectation.

1. The Numbers: Contactless by the Data

The data tells an unambiguous story — contactless is winning across every metric.

| Metric | 2022 | 2024 | 2026 | 2027 (Proj.) |

|---|---|---|---|---|

| In-person tap transactions | 38% | 52% | 62% | 71% |

| NFC-enabled terminals (U.S.) | 48% | 63% | 78% | 88% |

| Consumers who prefer tap | 55% | 72% | 85% | 90%+ |

| Digital wallet transactions ($B) | $86B | $180B | $320B | $450B |

| SoftPOS adoption (U.S. merchants) | <5% | 12% | 28% | 45% |

Source: Visa Digital Payments Report 2026, Mastercard Contactless Insights 2026, Nilson Report 2025–2026, Federal Reserve Payments Study 2025.

2. Why Contactless Matters to ISOs

Contactless adoption is not just a consumer trend — it directly impacts ISO revenue, merchant retention, and equipment strategy.

Contactless transactions take 3–5 seconds vs 15–25 seconds for chip dip. For a quick-service restaurant with 300 transactions/day, that saves 1+ hour per day in checkout time — directly increasing throughput.

By 2027, Visa and Mastercard will phase out support for non-NFC terminals at many merchant levels. ISOs who haven’t upgraded merchants by then face mass churn as merchants scramble.

Contactless digital wallet users spend 15–25% more per transaction than card-swipe users. Merchants with NFC terminals capture this premium.

Tap to Pay on iPhone/Android turns any smartphone into a payment terminal. ISOs can offer SoftPOS as a low-cost add-on for mobile merchants (food trucks, pop-ups, home services).

3. The Terminal Upgrade Playbook

ISOs need a proactive strategy for migrating merchants to NFC-enabled terminals. Here is the three-phase approach.

Phase 1: Audit (Q3 2026)

- Identify merchants still using non-NFC terminals (Verifone VX 520, Ingenico iPP 320, older Clover Mini units)

- Generate a simple report showing: “Your terminal supports insert/swipe only. 62% of your customers now expect to tap. You are losing 1 in 5 customers who prefer tapping.”

- Prioritize merchants in younger demographics (coffee shops, fast-casual, fitness studios)

Phase 2: Offer Upgrade Paths (Q4 2026–Q1 2027)

- Option A — Hardware refresh: $199–$399 for NFC-capable terminal (Clover Flex, Verifone P400, PAX A80)

- Option B — SoftPOS (zero hardware): $0 upfront; merchant uses their existing iPhone/Android with Tap to Pay; ISO earns $5–$15/month per device

- Option C — Subsidized upgrade: ISO covers terminal cost in exchange for 3-year contract extension and 0.1% rate increase

Phase 3: Capture Upsell Revenue (Ongoing)

- Add-on: contactless tipping (tap-to-tip increases tips by 30–50%)

- Add-on: loyalty via digital wallet (Apple Wallet/Google Pay integration)

- Add-on: NFC-capable customer-facing displays (CFD) for signature capture and feedback

4. SoftPOS: The Game-Changer

SoftPOS (software point of sale) — also known as Tap to Pay on iPhone/Android — is the fastest-growing contactless segment. And it creates a massive new merchant acquisition opportunity for ISOs.

| SoftPOS Option | Device | ISO Setup Fee | ISO Recurring |

|---|---|---|---|

| Tap to Pay on iPhone (Stripe) | iPhone | $0 | $5/mo per merchant |

| Tap to Pay on Android (Adyen) | Android | $0 | $3/mo per merchant |

| Clover Go (NFC+Mag) | Dedicated reader | $39 | $9.95/mo |

| SumUp (SoftPOS + card reader) | Phone + reader | $19 | $7/mo |

SoftPOS eliminates the upfront hardware cost barrier — the #1 blocker for new merchant acquisition. ISOs who bundle SoftPOS as a “terminal-free starter package” can onboard merchants in 24 hours instead of 2 weeks.

5. Common Merchant Objections & How to Handle Them

❓ “My current terminal works fine — why upgrade?”

“62% of your customers now tap. The ones who don’t see a tap reader are walking to the competitor down the street. Plus, Visa is phasing out non-NFC support by 2027 — your terminal will soon be non-compliant.”

❓ “Isn’t NFC more expensive for me?”

“Actually, NFC transactions have lower fraud rates than swiped (magnetic stripe) transactions. Less fraud means fewer chargeback fees. Net-net, merchants typically save $200–$500/year per terminal after switching.”

❓ “My customers don’t use Apple Pay”

“85% of U.S. consumers prefer tap. Even if your current customer base skews older, younger customers will avoid stores without tap. You are signaling ‘outdated’ to every new customer who walks in.”

❓ “Do I really need SoftPOS if I have a terminal?”

“SoftPOS is a backup, not a replacement. If your main terminal fails, your iPhone can immediately process payments. It also lets you take payments anywhere in the store — line-busting during peak hours, curbside pickup, or events.”

6. The ISO Revenue Math

Every terminal you upgrade generates measurable revenue upside for your ISO business:

| Revenue Source | Per Terminal/Year | 100 Terminal Book |

|---|---|---|

| Hardware markup (one-time) | $50–$150 | $5K–$15K |

| Processing lift (higher avg ticket) | $120–$400 | $12K–$40K |

| SoftPOS subscription (per device) | $60–$180 | $6K–$18K |

| Total Incremental Revenue | $230–$730 | $23K–$73K |

Bottom Line

Contactless is no longer a competitive advantage — it is table stakes. By 2028, merchants without NFC terminals will be as rare as stores that don’t accept credit cards. Every ISO has a narrow window (2026–2027) to upgrade their merchant book and capture the SoftPOS revenue opportunity before the market saturates.

Start your terminal audit today. Every merchant you upgrade now is a merchant you keep for the next five years.

📊 Data sources: Visa Digital Payments Report 2026, Mastercard Contactless Insights 2026, Nilson Report 2025–2026, Federal Reserve Payments Study 2025, Stripe/Adyen published SoftPOS pricing. Statistics reflect U.S. market as of Q1 2026.